Todd's Blog

-

Stock Market Got You Down? Good News: Home Prices Are Up!

- The repayment is limited to the gain on the sale of the home. Gain is typically computed by subtracting the original cost and improvements from the sales price;

- The home is destroyed or condemned, and a new home is purchased;

- Extended duty of military personnel or intelligence officials;

- Death of the taxpayer.

- Apply for a loan: Your ABR can help you understand the pre-application steps, the information your lender needs, the decisions you will have to make at application, the application costs and the application legal requirements.

- Closing costs and The Truth In Lending Statement: Mortgage costs include appraisal and points (a fee based on the amount of the loan). Depending on the loan, you may also be required to pay for mortgage insurance. To help you see everything you?re paying for the length of the mortgage, you will receive a Truth in Lending Statement, which is a good-faith estimate of all of the costs associated with the mortgage.

- Application and lender requirements: Includes social security number, date of birth, photo identification card, paycheck, W-2 or 1099 tax form, employers, accounts, current assets, liabilities, current and previous addresses, sales contract.

- Special situations: Lenders may require additional information if you are: self-employed, compensated on a commissioned basis, separated or divorced, social security/pension/disability/any form of public assistance benefits considered as income, bankruptcy/foreclosure or any judgments against you in the past 7 years, Department of Veterans Affairs (VA) Loan Application.

- Other considerations: Be sure to consider points and rate options and keep in mind that your financial position must be the same at closing as it was when you were approved (don?t buy a new car or purchase anything major!).

- Obtain homeowners insurance: Before closing, your mortgage will require you to obtain homeowners insurance. Costs and coverage will vary.

- Escrow accounts: Decide if you want to pay your property taxes and homeowners insurance policy on your own or if you would rather wrap them into your monthly mortgage payments.

- Completing a home inspection

- Requesting an attorney review

- Finalizing your mortgage

- Getting ready to move

- Attending a final walk-through

- Preparing to pay closing costs

- You, the buyer

- The seller

- The closing agent, the title insurance representative and the escrow agent (one person may fill all these roles)

- The real estate agents

- Attorneys for the buyer and seller

- The closing statement

- The mortgage papers

- A Truth in Lending Statement

- Any additional documents required in your state

- Determine cost of moving: Many people are surprised by the variety of expenses associated with moving, including packing materials, utility connections, insurance, cost of movers, truck rental, etc. You can eliminate or reduce these costs by investigating moving companies, estimating moving costs and making a moving checklist.

- Moving coverage: Before you select a mover to help you, confirm that the company is insured and provides coverage for your belongings. Three of the most common forms of insurance coverage are basic liability, declared value protection or actual cash value and replacement value.

- Packing tips:

- Determine credit status

- Select a lender

- Determine interest rates and duration

- Pre-qualify for a mortgage and get pre-approved before you find your home

- Determine how much you can affordOffer down payment and mortgage insurance

- Basic criteria (i.e. ideal price, total square footage, type of home, number of bedrooms, number of garages, number of bathrooms, etc.)

- Other home preferences (i.e. age of home, style of home, energy efficiency, floor plans, high priority home features, specialty rooms, storage needs, etc.)

- Location (preferred areas/communities, commuting considerations, proximity to desirable features, views, etc.)

- Lot characteristics (size and shape, landscaping considerations, home orientation)

- Life at home: Take children, pets, live-in parents and others into consideration

- Trade-offs: If you can?t find what you want, how much are you willing to invest to pay for improvements? Are you willing to consider other neighborhoods that offer better affordability?

- Resale: How long do you plan to live in this home?

- Neighborhood Profile: Research population density and level of commercial development

- Household Data: Family type, average household income and homeowner education level/occupation

- Crime Rate

- Quality of Schools

- Amenities (i.e. shopping, transportation, parks and recreation, restaurants, nightlife, etc.)

- Accept: You will have a binding contract as soon as you are notified of the offer?s acceptance.

- Reject: You are released of any obligation. The sellers cannot change their minds.

- Counteroffer: A seller may present a written counteroffer that includes the changes they want to make. You are free to accept, reject or make a counteroffer to their counteroffer.

- These 5 steps will help you choose and buy your new home. But wait! There are 5 more steps to the home-buying process coming up next in PART 2 of this blog series. Stay tuned for the next 5 steps including obtaining a mortgage, preparing for closing day, closing, moving and (of course) celebrating!

- Have fractures in the foundation, which allows gases to travel through underground channels

- Leave windows open often

- Utilize attic fans

- Have high traffic in and out of the home

- Are geographically located where droughts are prevalent

- Soils and basement footings that shift

- New furnace

- New air conditioning system

- Altered plumbing

- Improved insulation

- Structural additions to a home

- What is causing the energy loss?

- Is there anything dangerous or unhealthy in the home?

- Where are the potential health issues?

- What are the long-term building performance and durability issues?

- What times will be the most cost-effective to improve the home?

- High energy bills

- Air leaks

- Inefficient windows

- Missing insulation

- Inefficient cooling/heating equipment

- Poorly insulated ducts

- Mold and mildew

- High humidity and water damage

- Dust

- Hot/cold rooms

- Insulation

- Air leaks

- Medical costs by reducing:

- Indoor allergens

- Dust

- Mold

- Mildew

- Pests

- Reduce reliance on foreign natural gas and other fuels

- Cost: $1,201

- Resale value: $913

- Cost recouped: 76.0%

- Cost: $10,152

- Resale value: $7,231

- Cost recouped: 71.2%

- Cost: $16,026

- Resale value: $11,356

- Cost recouped: 70.9%

- Cost: $1,551

- Resale value: $1,048

- Cost recouped: 67.6%

- Cost: $2,834

- Resale value: $1,853

- Cost recouped: 65.4%

- Cost: $10,299

- Resale value: $6,718

- Cost recouped: 65.2%

- Cost: $11,193

- Resale value: $7,225

- Cost recouped: 64.6%

- Cost: $19,539

- Resale value: $12,474

- Cost recouped: 63.8%

- Cost: $12,142

- Resale value: $7,378

- Cost recouped: 60.8%

- Cost: $51,932

- Resale value: $31,314

- Cost recouped: 60.3%

- The bill was signed into law by President Obama on January 2, 2013.

- Mortgage Cancellation Relief is extended for one year to January 1, 2014.

- Deduction for Mortgage Insurance Premiums for filers making below $110,000 is extended through 2013 and made retroactive to cover 2012.

- 15-year straight-line cost recovery for qualified leasehold improvements on commercial properties is extended through 2013 and made retroactive to cover 2012.

- 10 percent tax credit (up to $500) for homeowners for energy improvements to existing homes is extended through 2013 and made retroactive to cover 2012.

- First and foremost, take safety precautions. Keep in mind that the water flowing into your home may be contaminated and should not be used until advised so. Be mindful of trees and other structures that could be unstable around your house.

- Secondly, seek medical attention if needed. Make sure that emergency services are able to get to your house or provide them with a safe alternate route in order to get there. Always keep in mind where power lines and bridges are located.

- Next, safeguard your property. Assemble your most prized possessions and find a safe place for them.

- Contact your insurance company. Take the time to fully understand what your homeowners or renters insurance policy does and does not cover.

- Next, contact your creditors. Make sure that your creditors are fully aware of what has happened and provide them with a temporary address if possible.

- Finally, it?s time to do one of two things?repair or relocate.

- MYTH: Tax will affect all homes or even most home sales. FACT: It is not a tax on total sales price. It is also not a sales tax.

- MYTH: The National Association of Realtors is working to get the tax repealed. FACT: The association, instead, is trying to counteract what people call ?grossly inaccurate? rumors about the levy.

- MYTH: The tax will only affect the very rich. FACT: In some circumstances, the tax could affect people who are not considered extremely wealthy.

- Has never owned a house, or as not owned a house in the past 3 years OR

- Is a single parent who is unmarried or legally separator with one or more minor children for whom the individual has custody or join custody, or is pregnant

- Is a displaced homemaker who is an adult who has not worked full-time for a full year in the labor force for a number of years, but has, during such years, worked primarily without remuneration to care for the home and family; and is unemployed or underemployed and is experiencing difficulty in obtaining or upgrading employment

- Has an income less than the income limits displayed on this chart.

- Live in the newly purchased home for at least five years

- Complete mandatory homeowner training including homeownership counseling sessions

- Use the home as a primary resident

- Occupy the home within 30 days of loan closing

- Have more than 30% liquid assets of total purchase price of home

- Have a down payment equal to 1% of the sales price (or $500)

- Stay under 41% of gross income for Total House Payment (PITI) plus recurring debt

- Down payment and closing cost assistance not to exceed $10,000 in the form of a deferred loan will be provided on behalf of the qualified participant.

- The home must be purchased in Johnson County.

- The home must be inspected by Johnson County Housing Rehabilitation Specialist and pass all Housing Quality Standards.

- The home must go under an environmental review by the Johnson County Housing Services office.

- For homes build before 1978, a lead-based paint report must be submitted to Johnson County Housing Services with the real estate sales contract.

- Buyers of properties located within 2,500 feet of the Johnson County Executive Airport are required to execute an affidavit acknowledging that they are aware of the proximity to the airport.

- A fixed mortgage rate of 15-30 year term.

- Interested rate cannot be more than 1.5% over FHA rate.

- Participant must purchase Private Mortgage Insurance (PMI) ? if lender requires.

- Purchase price must not exceed $204,250 (HUD guidelines).

After a slow start in the beginning of 2015, home sales have

grown significantly throughout the summer season. This summer, and the next few

months, will be a seller?s market. A surge in home sales driven by low rates

have led to tighter inventory and price gains. In 2014, the median home price

for 2014 was $208,500. In June 2015, on the other hand, the median monthly home

price was $236,400.

So if the stock market?s got you down these past few months,

look at the silver lining?home prices are up and a seller?s dream has emerged.

Learn more about the state of the real estate market in this recent

article from Keller Williams.

If you?d like a report on the value of your home, contact me right away.

If you?d like a report on the value of your home, contact me right away.

First-time Home buyers, Look into a 3% Down Conventional Loan

First-time home buying* just got easier and more affordable.

There is a new type of loan out there that may be of interest. It?s the 3% down

conventional loan, and it?s doing wonders for first-time home buyers like you.

*I have to preface

this blog post with a strict definition of what a ?first-time home buyer? is.

Only those who have not owned any property in the past 3 years are considered a

?first-time home buyer? and qualify for this type of loan. If two people are

buying the home, only one needs to be a first-time home buyer.

Most recently, the loans most first-time home buyers have

been selecting was either a 5% down conventional loan or an FHA loan requiring

a 3.5% down payment. Now that the 3% down conventional loan is available buying

a home has become a little easier and more affordable for first time

buyers. So, if you?d like to own a

home, you owe it to yourself to see if you qualify.

First of all, what is the 3% down conventional loan? This

loan is a better alternative to both an FHA loan (where you put 3.5% down) and

a standard 5% conventional loan because it allows you to qualify with a lower down

payment and it makes your mortgage insurance (aka MIP or PMI) much cheaper.

Plus, once you reach 20% ownership of the property, it drops off without being

forced to refinance.

I consulted with Chad Trease, Senior Loan Officer at Prime Lending for more information.

?This is a great alternative loan through the Fannie and

Freddie guidelines,? he explains. ?This loan may open the gates for more

homeowners.? Plus, according to Forbes,

the 3% down payment conventional mortgage financing ?does not handcuff

borrowers to mortgage insurance forever like FHA MIP does.?

First-time homeowners still have the ability to utilize a 5%

down conventional loan or an FHA loan to purchase their home but the 3% down

loan maybe a better option. In addition, both the 5% and 3% down payments can

be gifted if need be, allowing for even more flexibility.

First-time home buyers, now that buying a home is more

possible than ever before, it?s time to contact me to schedule a

consultation and learn more. Join me and Chad at our

first-time homebuyers seminar on February 26 at 6:30pm at 11005 Metcalf Ave. in Overland Park to get even more helpful

information about buying a home.

FHA Property Flipping Waiver Expires?What Does This Mean For First-time Homebuyers?

On December 31, the FHA announced that the property

flipping waiver had expired. The waiver prohibited the use of FHA financing

on the purchase of a single-family property that was resold within 90 days of

the previous acquisition. So now that the waiver has been expired, what does

this mean for first-time homebuyers?

I sought out the professional opinion of Chad Trease, Senior

Loan Officer at Prime Lending. ?Now

that the 90 day waiver has gone away,? explains Chad, ?it is going to be hard

to buy a house that was recently flipped.? He explained that any home that has been

flipped will not be eligible for FHA financing until its 91st day.

Is this a problem? According to Chad, probably not. ?Most flips

take longer than 90 days,? he explains. The reason for this action from the FHA

is to do away with people who purchase a home, do little to no work on it, and

try to sell the property for even more money right away.

First-time homebuyers need to be aware of this change,

especially when out in the market looking to purchase a home. First-time

homebuyers should also be aware that although you cannot use an FHA loan until

after 90 days, you can use a

conventional loan.

Almost anyone qualifies for an FHA loan, however, you are

only allowed to have one at a time. FHA loans typically have very expensive

mortgage insurance that never drops off the loan. According to Chad, an FHA

loan is ideal for homebuyers who are credit challenged. In other words, it?s

somewhat of a last resort. Conventional loans, on the other hand, are for

first-time homebuyers who have not owned property in the prior 3 years.

Conventional loans have a lesser down payment and have a cheaper mortgage

insurance that drops off once you reach 20% of the property.

First-time homebuyers, keep in mind that it is not common

for a homebuyer to purchase a flipped home before the 90-day timeline. As

mentioned before, most flipped houses take longer than 90 days to complete.

However, if you have further questions or concerns, contact

me and we can talk through the details.

Did You Purchase a Home in 2008? What You Need to Know

Individuals who purchased a home in 2008 and took advantage of the First Time Homebuyer Tax Credit?keep reading. I consulted with Ryan L. Ross, CPA at the Leawood Office Business Center in Leawood, Kansas. He provided some insight into what you need to know as a seller who purchased their home in 2008 and claimed a credit.

First, for all homes purchased in

2008, the First-Time Homebuyer Credit is repaid over 15 years or sooner if the

home is sold or ceased to be the taxpayer?s main home. For homes purchased

after December 31, 2008, the credit must be repaid only if the home is sold or

ceases to be the taxpayer?s main home within 36 months of the date of purchase.

Other things to note: Form 5405,

Repayment of the First-Time Homebuyer Credit, must be filed for the year the

home is sold or ceases to be the taxpayer?s main home.

Be sure to look into exceptions to

this repayment rule, too. These exceptions include:

For more information, consult your

tax advisor or contact me

to get in touch with someone who can help.

The Numbers Are In! 2014?s Remodeling Projects With the Highest Cost Recouped in Kansas City

Last year, I published a

blog titled The Top 10 Remodeling Projects with the Highest Cost

Recouped in Kansas City that covered the home remodeling projects that gave homeowners the

highest rate of return in 2013. Now that 2013 has come and gone, it?s time to

see which remodeling projects will give you the best return on investment in

2014!

According to Remodeling, the top

10 remodeling projects with the highest cost

recouped in Kansas City this year are:

1. Garage Door Replacement:

Remove

and dispose of existing 16x7-foot garage door and tracks. Install new 4-section

garage door on new galvanized steel tracks; reuse existing motorized opener.

New door is uninsulated, single-layer, embossed steel with two coats of

baked-on paint, galvanized steel hinges, and nylon rollers. 10-year limited

warranty.

Cost: $1,604

Resale value: $1,233

Cost recouped: 77.0%

2. Minor Kitchen Remodel:

Cost: $1,604

Resale value: $1,233

Cost recouped: 77.0%

2. Minor Kitchen Remodel:

In a functional but

dated 200-square-foot kitchen with 30 linear feet of cabinetry and countertops,

leave cabinet boxes in place but replace fronts with new raised-panel wood

doors and drawers, including new hardware. Replace wall oven and cooktop with

new energy-efficient models. Replace laminate countertops; install midpriced

sink and faucet. Repaint trim, add wall covering, and remove and replace

resilient flooring.

Cost: $19,854

Resale value: $14,941

Cost recouped: 75.3%

3. Entry Door Replacement (Steel):

Cost: $19,854

Resale value: $14,941

Cost recouped: 75.3%

3. Entry Door Replacement (Steel):

Remove existing 3-0/6-8

entry door and jambs and replace with new 20-gauge steel unit, including clear

dual-pane half-glass panel, jambs, and aluminum threshold with composite stop.

Door is factory finished with same color both sides. Exterior brick-mold and

2.5-inch interior colonial or ranch casings in poplar or equal prefinished to

match door color. Replace existing lockset with new bored-lock in brass or

antique-brass finish.

Cost: $1,240

Resale value: $837

Cost recouped: 67.5%

4. Deck Addition (Wood):

Cost: $1,240

Resale value: $837

Cost recouped: 67.5%

4. Deck Addition (Wood):

Add a 16-by-20-foot deck

using pressure-treated joists supported by 4x4 posts anchored to concrete

piers. Install pressure-treated deck boards in a simple linear pattern. Include

a built-in bench and planter of the same decking material. Include stairs,

assuming three steps to grade. Provide a complete railing system using

pressure-treated wood posts, railings, and balusters.

Cost: $10,311

Resale value: $6,926

Cost recouped: 67.2%

5. Bathroom Remodel:

Cost: $10,311

Resale value: $6,926

Cost recouped: 67.2%

5. Bathroom Remodel:

Update an existing

5-by-7-foot bathroom. Replace all fixtures to include 30-by-60-inch

porcelain-on-steel tub with 4-by-4-inch ceramic tile surround; new single-lever

temperature and pressure-balanced shower control; standard white toilet;

solid-surface vanity counter with integral sink; recessed medicine cabinet with

light; ceramic tile floor; vinyl wallpaper.

Cost: $17,439

Resale value: $11,444

Cost recouped: 65.6%

6. Two-story

Addition:

Add a first-floor family

room and a second-floor bedroom with full bathroom in a 24-by-16-foot two-story

wing over a crawlspace. Add new HVAC system to handle addition; electrical

wiring to code.

Family room: Include

a prefabricated gas fireplace; 11 3-by-5-foot double-hung insulated clad-wood

windows; an atrium-style exterior door; carpeted floors; painted drywall on

walls and ceiling; and painted trim.

Bathroom: 5

by 8 feet. Include a one-piece fiberglass tub/shower unit; standard white

toilet; wood vanity with solid-surface countertop; resilient vinyl flooring;

and mirrored medicine cabinet with built-in light strip; papered walls; and painted

trim; exhaust fan. Bedroom: Include walk-in closet/dressing area; carpet;

painted walls, ceiling, and trim; general and spot lighting.

Cost: $165,580

Resale value: $106,054

Cost recouped: 64.1%

7. Deck Addition (Composite):

Cost: $165,580

Resale value: $106,054

Cost recouped: 64.1%

7. Deck Addition (Composite):

Add a 16-by-20-foot deck

using pressure-treated joists supported by 4x4 posts anchored to concrete

piers. Install composite deck material in a simple linear pattern. Include a

built-in bench and planter of the same decking material. Include stairs,

assuming three steps to grade. Provide a complete railing using a matching

system made of the same composite as the decking material.

Cost: $16,291

Resale value: $10,297

Cost recouped: 63.2%

8. Siding Replacement (Vinyl):

Cost: $16,291

Resale value: $10,297

Cost recouped: 63.2%

8. Siding Replacement (Vinyl):

Replace 1,250 square feet of existing siding

with new vinyl siding, including all trim.

Cost: $12,411

Resale value: $7,803

Cost recouped: 62.9%

9. Major Kitchen Remodel:

Cost: $12,411

Resale value: $7,803

Cost recouped: 62.9%

9. Major Kitchen Remodel:

Update an outmoded 200-square-foot kitchen with

a functional layout of 30 linear feet of semi-custom wood cabinets, including a

3-by-5-foot island; laminate countertops; and standard double-tub

stainless-steel sink with standard single-lever faucet. Include

energy-efficient wall oven, cooktop, ventilation system, built-in microwave,

dishwasher, garbage disposal, and custom lighting. Add new resilient flooring.

Finish with painted walls, trim, and ceiling.

Cost: $57,520

Resale value: $36,044

Cost recouped: 62.7%

10. Attic Bedroom:

Cost: $57,520

Resale value: $36,044

Cost recouped: 62.7%

10. Attic Bedroom:

Convert unfinished attic space to a

15-by-15-foot bedroom and a 5-by-7-foot bathroom with shower. Include a 15-foot

shed dormer, four new windows, and closet space under the eaves. Insulate and

finish ceiling and walls. Carpet floor. Extend existing HVAC to new space;

provide electrical wiring and lighting to code. Retain existing stairs, but add

rail and baluster around stairwell.

Cost: $53,696

Resale value: $32,371

Cost recouped: 60.3%

Cost: $53,696

Resale value: $32,371

Cost recouped: 60.3%

Want

to learn more about buying or selling a home in the Kansas City and Overland

Park areas? Check out my Facebook page.

January is Radon Awareness Month ? Get Your Home Tested For Only $100!

Image credit: Shane Lyle, Geology Extension

Kansas Geological Survey

January has been designated as Radon Awareness Month by the United States Environmental Protection Agency. But as a

homeowner, do you even know what radon is?

I caught up with my good friend

John Clason with Crown

Home Inspections to learn a little bit more. In honor of Radon Awareness Month, John

isn?t just inspecting homes for their radon levels, he?s doing it at a

discounted price!

Before I let you in on the discount

details, let?s explore what radon is and why your home may need to be tested.

As mentioned in a previous

Team Ohlde blog post, radon is a silent and odorless

gas that could leak into homes from the natural decay of uranium present in

different types of soil. Radon contains cancer-causing alpha particles that are

drawn from parched soil through draught-driven cracks in home foundation.

Believe it or not, radon is the second leading cause of lung cancer, only

behind smoking. The EPA estimates that approximately 22,000 people die each

year from lung cancer caused by radon.

So as you can infer, having high

radon levels in your home can be extremely dangerous. But the even scarier part

is that it?s almost impossible to tell what radon levels your home has unless

you do a radon test. A radon tests

includes a 48-hour moderation of the home. John at Crown Home Inspections uses

an electric continue radon monitor that tells the radon level for each hour

during the test and provides an overall reading at the end.

After the test, homeowners receive

an overview of their home?s radon levels. Any home with a radon level of 4.0

picocuries per liter of air or higher should act immediately. Luckily, it?s easy to fix any high

levels of radon.

What?s the fix exactly? A radon mitigation system can be

installed in a home in about 3-4 hours.

As the cliché phrase goes, it?s

better to be safe than sorry! Take the month of January to schedule a radon

testing for your home from Crown Home Inspections for just $100 (a $25 discount

off the regular price through February 15, 2014!). Visit Crown

Home Inspections website to learn more.

Want more help with keeping your

home safe and in shape? Check out my list of local services providers! Click

here.

Fannie Mae Changes Guides on Gift Funds

Lately, I?ve been getting quite a few questions from

homebuyers about the major changes to Fannie

Mae (FNMA). For starters,

allow me to define Fannie Mae: Fannie Mae is a government-sponsored enterprise

that primarily buys mortgages from lenders for cash or pools them and sells

them as mortgage-backed securities to investors on the open market.

So what?s changing about FNMA? Like most industries, nothing stays the same for long?and

real estate is no exception. There

are many changes coming along that will affect homebuyers in 2014 and one of

those is a new FNMA rule with gift down payments.

In the past, most homebuyers have not had the opportunity

to use 100% ?gift

funds? (a financial gift from a spouse or other blood relative, even

one?s employer) for their down payment.

So many used the 3% down Conventional (97 LTV) or 3.5% down FHA option,

100% gift (96.5 LTV) options when purchasing a home or they would use a

conventional loan with 5% down. But because of major changes to the real estate

market, FNMA is now allowing homebuyers to use gift funds to make their 5% down

payment on a conventional loan, making the 5% (95 LTV) option much more

attainable, particularly for first-time home buyers.

So what does this mean for homebuyers exactly? A whole lot of opportunity. In order to get an understanding of this

change, I talked with Jim Griffiths, a Mortgage Advisor at Stonegate

Mortgage.

?There really is no downside to this change for borrowers,?

explains Jim. ?While the 3% down

option went away, this allows more home buyers access to conventional lending programs. It?s

perfect for first-time homebuyers who may not have had enough time to save up

enough of their own cash reserves to make a down payment. They can really use this to their

advantage.?

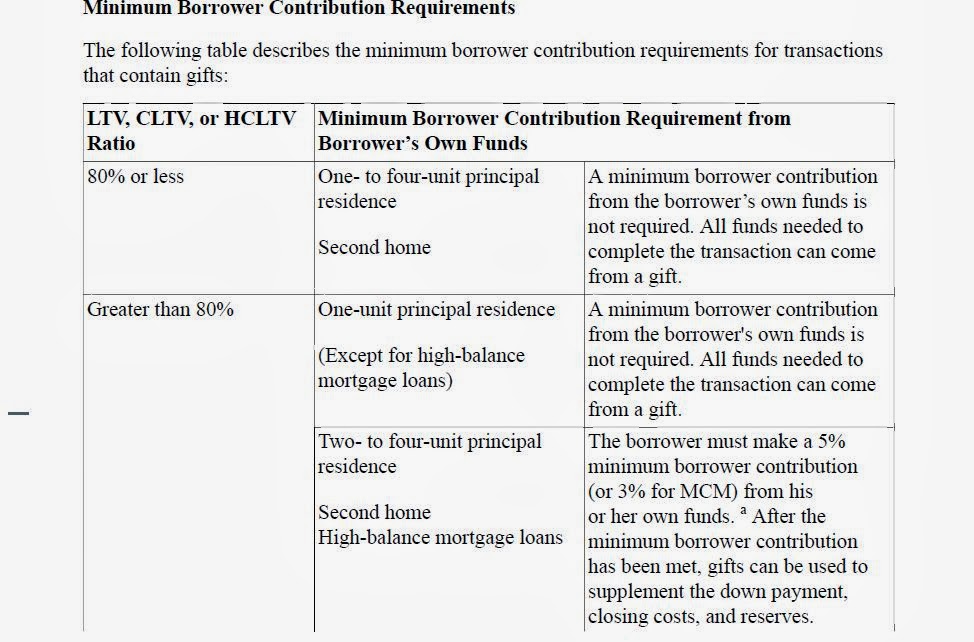

The table below will help homebuyers further understand this

change and see the minimum borrower contribution requirements for transactions

that contain gifts:

As Griffiths stated, with this

change, homebuyers are putting more skin in the game, not to mention more

investment in the market. The

message here is that investors want to see more ?skin in the game? even though

it may be 100% gifted funds.

?Bottom line, if someone can help you with

your 5% down payment, you now have that option,? says Griffiths. ?Conventional lending provides a much

less expensive option from a mortgage insurance perspective, which lowers the

overall monthly payment. In the

long run, it can also be cheaper than an FHA loan. My recommendation is that if

it?s available, take advantage of it.?

If you would like to take advantage of this new loan opportunity and begin the home buying process, please contact me today to schedule a private consultation.

Phone: 913.568.7355

Email: [email protected]

Website: www.toddohlde.com

Or, if you have more questions regarding the new Fannie Mae guides, or if you want to inquire about qualifying for a home loan, please contact Jim Griffiths:

Phone: 913.951.3786

Email: [email protected]

Want more tips and breaking

news about the housing market? Stay posted on my Facebook page or contact me.

10 Steps to Choosing and Purchasing Your Home (PART 2)

Be sure to check out PART 1 here!

So you are ready to buy a home. It?s a big decision and there?s a lot to

learn. But with these 10 quick steps,

choosing and purchasing your home will be easier and more seamless than ever

before. This guide provides 10 key steps, information and tools in order for

you to find, purchase and finance a home that meets your needs and preferences.

In a previous blog, I discussed the first 5 steps in helping

you choose and purchase your home. You

can read that blog here. Now,

it?s time to discuss the last 5 steps so you can finalize that home purchase

and get to the celebrating!

STEP 6: Obtain a Mortgage

Securing a mortgage is

oftentimes more complex and more expensive than a consumer may realize. That?s why it?s important to be organized and

find a competent mortgage loan officer.

Your ABR (Accredited Buyer?s

Representative) has already helped other buyers work through the mortgage

application process and can also provide valuable assistance.

How to obtain

a mortgage:

STEP 7: Prepare for

Closing Day

Many important details must fall in place before you close on

your home. Your ABR will help you stay

on track. The most important details

include:

STEP 8: Close

The actual, legal transfer of ownership is called closing or settlement. Participants of the closing usually include:

During the meeting, you?ll sign many documents including:

Be prepared to provide your payment of closing costs, proof

of insurance and approval of inspections, too!

STEP 9: Move

You found your home!

The contract has been signed! The

closing date is set! Now it?s time to

move. Be sure to plan for the moving day

well in advance with these helpful tips:

o

Begin packing as early as possible

o

When packing, go room by room

o

Make a list of what?s in each box

o

Label all boxes by room

o

Cushion the bottom and sides of boxes

o

Pack heavy items in smaller boxes

o

Packed boxes should not exceed 30 lbs

o

Fill you washer/dryer with clothes, linens and

light items

o

Wrap and secure cords

o

Use rope or elastic to secure doors and drawers

o

Let the children help!

STEP 10: Celebrate!

Congratulations!

You?ve worked hard to achieve your dream of homeownership. I would like to wish you many years of happiness

in your home. Cheers!

Want

to learn more? You can receive your own

home buyer?s toolkit at www.toddohlde.com. Click on Contact Me to send me

an email and request your copy. All you

have to do is provide me with your home address. It?s as easy as that!

10 Steps to Choosing and Purchasing Your Home (PART 1)

So you are ready to buy a home. It?s a big decision and there?s a lot to

learn. But with these 10 quick steps,

choosing and purchasing your home will be easier and more seamless than ever

before. This guide provides 10 key steps, information and tools in order for

you to find, purchase and finance a home that meets your needs and preferences.

Below are the first 5 steps to get you started. Stay tuned for PART 2 where I will unveil the

next 5 steps to keep in mind when choosing and purchasing a home!

STEP 1: Find a

Qualified Buyer?s Representative

How often do you purchase real estate? Once, twice, three times in your

lifetime? So you can hardly be expected

to know all the ins and outs of such a major transaction complicated by so many

details. That?s when a qualified buyer?s

representative comes in handy.

What is a

buyer?s representative? A

buyer?s representative (also known as a buyer?s agent) is an advocate for the

buyer--not the seller--in a real estate transaction.

Why should

you use a buyer?s representative? A

buyer?s representative can provide the expertise you need throughout the entire

transaction, greatly improving your buying experience and potential

results. Plus, retaining a buyer?s

representative seldom adds any expense to your transaction!

Why choose an

Accredited Buyer?s Representative? A REALTOR with the ABR designation has completed Accredited Buyer?s Representative training,

specialized education offered by the Real Estate Buyer?s Agent Council (REBAC). REALTORS with the

ABR designation understand the special needs of buyers. They have additional knowledge and experience

that takes them a step beyond an agent who only concentrates on listing

property for sellers.

What issues

should you discuss? After

narrowing down your favorite ABR agents, be sure to ask some questions. This will help you make your final decision. Topic questions include experience and

credentials, references, knowledge, representation, services provided,

compensation, finding properties, personal support, negotiating, financing and

related service providers.

Once you?ve found your

ABR, you can discuss compensation (usually commission to the buyer?s agent) and

then you may begin working as a team!

STEP 2: Assess Your

Credit and Finances

Financial considerations and preparations are central to any

home purchase. In addition to helping

you make better decisions about what you can afford in a home, a buyer who

already has financing in place is in a better negotiating position when it?s

time to make an offer.

Assessing your credit card and finances can be broken down

into 6 steps. Be sure to check off each

step before you purchase a home:

STEP 3: Asses Your

Wants and Needs in a Home

Deciding what you truly want, need and can afford in a home

can be challenging. But your ABR can

play a key role in helping you sort out your options. The following preferences should be discussed

with your ABR before you purchase a home:

STEP 4: Search for

Your Home

Your ABR can direct you to helpful sources of information for

evaluating neighborhoods (although due to Federal Fair Housing Laws, they can?t

tell you everything you want to

know). When evaluating a neighborhood,

keep the following in mind:

After selecting a neighborhood, it?s time to view

houses! You can view homes on your own

(at Open Houses, for example) or with help.

Remember that your ABR will help you refine your search if you can?t find

what you?re looking for. To get started,

I suggest searching my website on the Home Search page

to find your next home. Another great

resource is REALTOR.com.

This site provides online information on millions of properties,

neighborhoods and other topics.

STEP 5: Negotiate Terms

You found your home.

Now it?s time to make an offer.

Lucky for you, your ABR can provide valuable assistance on this

regard--counseling you on market conditions, price ranges and negotiation

strategies.

How do I

start to negotiate? First,

your ABR will perform a comparative market analysis (CMA) on the

property. This will give you a better sense of whether the seller?s listing

price is higher or lower compared to other properties. Other negotiation considerations include if

you?re an all-cash buyer, if you are pre-approved for a mortgage and if you do

not have to sell your current home before you can complete the purchase.

How do I make an offer? An

offer must be a written contract. Your

ABR will help you use a standard form that is up-to-date with changing real

estate laws. Your ABR will also help you

structure your offer and negotiation strategy.

Purchasing offers contain a lot of information. Keep in mind that the more you demand, the

less favorably the sellers may look on your offer.

What about

contingencies? A contingency is a term

that must be met for an offer to become a binding contract. They always weaken the offer, but some are

considered normal. Common purchase offer

contingencies include approval of agreed-upon third-party inspections,

obtaining specific financing terms, securing a specific job or selling your

current home.

What about

earnest money? Earnest money is a cash deposit you make when

submitting your written offer on a property to show your ?good faith?.

What are

seller disclosures? Many areas

require sellers to disclose any known material defects. Be sure to ask just in case. Read and understand all documents.

What if there

are multiple offers? Don?t panic

and immediately withdraw your offer. It

is quite possible that you have submitted the winning bid. Stay involved for at least one round of

negotiations, but also establish your maximum price.

What can a

seller?s response be? A seller?s

response will either be:

To

receive your own home buyer?s toolkit or to schedule a private consultation to

begin your search, visit www.toddohlde.com and click on

the Contact Me page. I look forward to hearing from you!

Kansas City Radon Levels on the Rise?What Should You Do?

There?s no denying it?the weather in Kansas City has been

out of control. One week we?re boasting

80 degree weather and the next, there?s a blizzard. But something that we may not have noted is

the severe

drought that the KC metro region is currently experiencing. As a matter of fact, we are about to enter

month 21 of a large Midwestern drought.

What does that mean for you?

Radon problems.

What is radon?

Radon is a

silent (and odorless) gas that can leak into homes from the natural decay of

uranium present in all different types of soil.

Radon contains cancer-causing alpha particles that are drawn from

parched soil through drought-driven cracks in home foundations. The US Environmental

Protection Agency has linked indoor radon to 20,000 lung-cancer deaths

annually.

Is radon in my home?

You are breathing in radon right now. And we?ve all been breathing it in since we

were born. It?s a natural process that

our bodies have learned to cope with.

It?s when we breathe in too much radon over a long period of time that

we need to be weary of. The homes with

the highest levels of radon:

Kansas City radon

levels

So if radon levels rise when a drought occurs, why is Kansas

City experiencing such high levels?

After all, there?s plenty of wet snow on the ground! As a matter of fact, despite the snow piles

that have taken over the city, no handful of wet-weather events can cancel

scientists? predictions on the drought and radon levels in Kansas City.

According to the Kansas

City Star, KC is one of the nation?s hottest spots for indoor radon levels

above what federal authorities consider safe.

Between 33% and 45% of Kansas City homes show radon levels higher than 4

picocuries per liter (the average home tests at a safe 1.3 pCi/L).

Preventing &

testing radon levels

How can you prevent high levels of radon in your home? It?s actually quite simple! First and foremost, it?s important to note

that you should test your home approximately every 2 years. The best time to test for radon is in the

winter, when a home is sealed up and the furnaces are churning (so why not do

it today?).

In addition to bi-annual testing, the Kansas and Missouri

governments are taking action to fight off the chances of radon sickness. A bill

introduced this year in the Kansas Legislature will make radon testing

mandatory for every home sale. This bill

will also allow the state to compare the reported levels to health problems

diagnosed in residents. Currently,

Missouri is not introducing a bill to require radon testing.

So how much is this

going to cost me?

A DIY radon

testing kit can be purchased for less than $10 at your local home

improvement store. Once you have

purchased a kit, you may need an additional $10-$30 for lab tests. If you?d like professional advice, most

services cost around $100-$200 in the Kansas City area. If you decide to hire a professional, look

for companies certified by the state of Kansas for radon inspection (Missouri

does not have this requirement).

If you find that your home has over 4 pCi/L, it is time to

shop for a mitigation piping system.

These pipes, including installation, will run at about $700-$1,400. Always remember?it?s better to be safe than

sorry!

Your Home Should Go Green with an Energy Audit this St. Patrick?s Day

Is your home ?going green? this St. Patrick?s Day? If so, there is a process you should be aware

of?it?s known as the energy audit process.

What is an energy

audit?

An energy

audit is the correlation between how much energy your home is currently

using and how much it should be using.

Energy audits, which can be provided by certified energy auditors,

provide the best cost/benefit analysis for every savings opportunity

identified. At the end of the energy

audit process, you will receive a report that highlights any problems or

opportunities for you to start saving energy.

From there, you can check out recommendations and further actions in

order to turn your home into the green machine it needs to be!

What does an energy

audit solve?

An energy audit is the only way to make sure that if you

spend money on home improvements that you spend it in areas that will truly

give you back value on your dollar. The

entire energy audit process answers important questions such as:

What types of

problems will an energy audit find?

Energy audits find many different problems in the home such

as:

Team Ohlde recently spoke with Barry Dicker of Decent Energy, an

energy auditor in Kansas. According to

Barry, the real estate industry may change due to process like energy

audits. A new appendix has been written

in regards to the appraisal process.

Appraisers now have the ability to value the energy efficiency of

homes. Unfortunately, only 5% of appraisers

are actually trained to apply this appendix.

The team at Decent Energy, however, has experienced higher values in

homes that have gone through the energy audit process.

Finding an energy

auditor near you

So you?re ready for the energy audit process. Who should you contact? Lucky for you, I have three local KS and MO contacts

that would provide a great starting point to bring your home the energy

efficiency it needs:

Home Green Home Energy Audits is a premier energy auditor

for the Greater Kansas City metropolitan area including Raytown, Lee?s Summit,

Independence, Blue Springs, Belton and Raymore in both Missouri and

Kansas. Home Green Home Energy Audits

provides guaranteed prices complete with insulating services, weatherization,

door and window replacement, plumbing, heating and air, remodeling

and more. Home Green Home Energy Audits

charges about $400 for homes under 4000 square feet and approximately $600 for

homes over 4000 square feet.

The Hayes Company, located at 1000 East 11th

Street in Kansas City, MO provides insulation and home performance solutions

throughout the greater KC metro area. A

home energy evaluation from The Hayes Company ranges from a free estimate to a

$150 walkthrough (with a blower-door

test) to a full-on $400 energy assessment.

The $400 assessment includes a pre-test and computer analysis that

calculates the savings in dollar amounts for each improvement recommended.

Decent Energy, based out of Leawood, Kansas, serves both

eastern Kansas and western Missouri commercial and residential energy

audits. Decent Energy works as an

independent auditor and therefore, works with the homeowner to find the best

contractors after the audit has been conducted.

The Decent Energy service includes a 13-month process of discussing

homeowner comfort issues, visual inspection, measurements, assessment of safety

zone issues and air leakage analysis with a blower-door tool. In addition, the team at Decent Energy retests

the home after the improvements have been made.

Decent Energy starts its service with a $550 baseline and then upcharges

for additional furnaces (rather than pricing by square foot).

The Top 10 Remodeling Projects with the Highest Cost Recouped in Kansas City

If you?ve got a fixer-upper or just want to make some improvements on your home, there are some areas that you should focus on first. Always take into consideration which remodeling projects will get you the highest rate of return. The higher the cost recouped, the better your remodeling investment was!

So which remodeling projects tend to have the highest cost

recouped here in Kansas City? We took at

look at the Remodeling 2013 Cost vs. Value

Report which gave us an in-depth look at what homeowners from KC should

focus on when it comes to remodeling.

The top 10 remodeling projects with the highest cost

recouped in Kansas City are:

1. Entry

Door Replacement (steel): This

remodeling project includes removing existing 3-0/6-8 entry door and jambs and

replacing them with a new 2-gauge steel unit, including clear dual-pane half

glass panel, jambs, and aluminum threshold with composite stop. It also includes replacing the existing

locket with a new bored-lock.

Top 4 Things Homeowners Need to Know About The Fiscal Cliff

The fiscal cliff. You may have heard of it and you may know what it is. But how does the fiscal cliff affect homeowners and the real estate industry? I have narrowed down the top 4 things homeowners need to know about the fiscal cliff in 2013:

1. It?s all about the dates.

There are some important dates that will affect you as a homeowner. But what day is important and what day isn?t? Here?s what you really need to remember:

2. Pease Limitations

Pease Limitations reduce the value of itemized deductions and are permanently repealed for most taxpayers. These will, however, be reinstituted for high income filers (individuals earning more than $250,000 and joint filers earning above $300,000). The amount of adjusted gross income above the threshold is multiplied by 3 percent, however, the total amount of reduction cannot exceed 80% of the filer?s itemized deductions.

3. Capital Gains

Capital Gains rate stays at 15% for those in the top rate of $400,000 (individual) and $450,000 (joint) return. After that, any gains above those amounts will be taxed at 20%. The $250,000/$500,000 exclusion for sale of principal residence remains in place.

4. Estate Tax

The first $5 million dollars in individual estates and $10 million for family estates are now exempted from the estate tax. After that the rate will be 40 percent, up from 35 percent. The exemption amounts are indexed for inflation.

To learn more about the fiscal cliff, be sure to visit the following resources:

Win a $200.00 or $50.00 Amex Gift Card from Team Ohlde!

During the holiday season, we all could use a little extra

cash. Lucky for you, that extra cash

could be in the palm of your hand...just by visiting Team Ohlde on Facebook!

On December 14, 2012, Team Ohlde will be giving away both a

$200.00 and a $50.00 American Express gift card?just in time for the

holidays!

How can you win? Simply ?Like? Team Ohlde on Facebook

before December 14, 2012 to enter to win!

Two lucky Facebook fans will be drawn on December 14th and

will win either a $200.00 or a $50.00 retail card from AMEX! It?s that simple!!

So what do you say?

Want to do a little extra fun shopping this holiday season? Like Team Ohlde on Facebook

and start your holidays off on the right foot!

Good luck!

Visit Team Ohlde: http://www.facebook.com/teamohlde?fref=ts & @ToddOhlde

The Impact of Natural Disasters on the Real Estate Market

The United States, and more specifically the Northeast states, are experiencing one of the largest hurricanes of all time. At about the same size as the state of Texas,

Hurricane

Sandy has blown through the Northeast coast, leaving many New Yorkers in

complete tragedy throughout the last few days of October 2012. Sandy has threatened an estimated 284,000

homes and has caused approximately $87 billion in damages, according to CoreLogic. Massapequa, located on the South Shore or

Long Island, has more than $4.6 billion in total structure value at risk alone.

The impact of what is now being referred to as ?Superstorm

Sandy? does not only affect many families in the New York area, but Inman

News has also reported that natural disasters, much like this one, can have

a ?chilling? effect on the real estate market.

How so?

When natural disasters occur in certain areas, home buyer

confidence greatly decreases. In

addition, these catastrophes have been proven to stall mortgage operations,

hurt home sales and have even more dire consequences when combined with the

current economic factors that our nation is experiencing.

Take one of the nation?s most famous hurricanes of all time,

for example?Hurricane Katrina. Hurricane Katrina did

more than kill more than 1,800 people and displace 750,000 households. In addition, the number of homes sold in New Orleans

dropped approximately 23% in just one year (May 2008-May 2009).

The same exact outcome was reported in the real estate

market after the 1989 and 1994 earthquakes in San Francisco. Even after the massive oil spill on the

Gulf Coast (although it was a man-made catastrophe rather than a natural

disaster), the market crashed. In fact,

the Gulf Coast oil spill impacted the real estate industry so much that $60

million of BP?s $20 billion Claims Fund was set aside for real estate

professionals.

But that?s not to say that all catastrophes have a negative impact on the real estate

market. One of the biggest surges in the

New York market happened immediately after 9/11. After the terrorist attack, many home buyers

took a stand against terrorism by purchasing even more homes in the beginning

of 2002.

Our homes mean everything to us?not only do they keep us

safe and provide us with shelter, but they also hold a some of our favorite memories. However, if you or your home

ever undergoes a natural disaster, there are a few steps to take to alleviate

the problem:

Natural disasters are an absolute tragedy and cannot be avoided. From hurricanes to tornadoes, floods to fires, earthquakes to eruptions, we never know what to

expect from Mother Nature. The best

thing to do during a time of natural disaster is to remain calm and stay

safe.

What is the 3.8% Tax on Investment Income?

It?s enough of a shock that 2012 is nearing its end. Where did the year go? As we finish up the last few months of this year, it?s important to note a new tax that will go into effect on January 1, 2013. It?s a brand new 3.8% tax on some investment income?and trust me, it?s a bit complicated.

How will this new tax affect your day-to-day life? What should you prepare for? And what do you really need to know about the 3.8% tax on investment income? Team Ohlde is here to answer all of your questions.

What is the 3.8% tax?

It?s a misconception that the 3.8% tax will be imposed on all real estate transactions. That is not the case. In fact, the tax that will begin on January 1, 2013 will impose tax on ?unearned income? such as investments, rental income and home sale profits over a certain exemption amount.

Myth vs. Fact

Recently, MSN Money put together a list of myths and facts about the 3.8% tax. Read on to find out what?s true and what?s false:

Does the 3.8% tax apply to everyone?

No?in fact, the tax will only fall on individuals with an adjusted gross income (or AGI) above $200,000. It also affects couples filing joint returns with more than $250,000 AGI.

Why is the 3.8% tax going into effect?

In 2010, Congress passed the 3.8% tax in order to generate an estimated $210 billion (over 10 years) to help fund President Barack Obama?s health care and Medicare overhaul plans.

So how will this affect me?

As mentioned earlier, the 3.8% tax will only affect those with over $200,000 AGI (or $250,000 AGI for couples). In addition, it will only tax income from interest, dividends, rents and capital gains. To view various scenarios of how this could potentially affect you, please read The 3.8% Tax: Real Estate Scenarios & Examples, distributed by the National Association of Realtors. The brochure will give insight to those looking for more information on capital gain, securities, rental income, sales of second homes, etc.

What should I do?

If you think you (or even your parents) could be subject to this new tax, it might be smart to sit down with a tax professional to talk about alternatives. Consider closing a home sale before December 31, 2012?or selling investments that could trigger the tax?that could save some money. The best next step is to meet with a tax professional to determine if action is necessary.

What is the real estate industry?s view on the tax?

As a matter of fact, the NAR expressed strong objections against the tax when it was first proposed in March of 2010. Legislation decided to pass the tax due to the party line vote. It's not true that the National Association of Realtors is working to get the tax repealed. In fact, the association has been trying to counteract what a spokeswoman called "grossly inaccurate" rumors about the levy.

Which Home Appliances Are Worth Upgrading?

With buzz words like ?energy efficiency? and brands like Energy Star are concepts often heard by homeowners, yet many are left wondering: which of my home appliances are actually worth upgrading? Is upgrading my appliances a waste of time or something I need to look into? How much will it cost to upgrade my appliances?

The questions go on and on...and sometimes the answers are not easy to find. Lucky for you, here at Team Ohlde, we know exactly which appliances are most important to upgrade in your home. Many appliances have made huge strides in the energy-saving world. Others, like small appliances, just aren?t worth upgrading all together. But did you know that 13% of your household?s energy costs come from appliances? Cutting your appliances energy usage will often save you money over time!

My advice? Upgrade the following appliances:

1. The Air Conditioner

We are all well aware that air conditioners tend to be very energy inefficient (especially in the summer!). Today?s modern retail air conditioners usually uphold a 10 EER rating (the higher the number, the more efficient it is), when 10 year old air conditioners rate at about a 7 EER. New Energy Star air conditioners usually run for about $220.00 when an Energy Star central air conditioner could run over $3,000 with installation.

Want a lower bill without investing in a new more energy efficient air conditioner? Simply replace the filters, clean the coils or manage the ducts?you?ll see your bill go down in no time!

2. The Furnace

Moving on to the opposite of the air conditioner?the furnace. Typical furnaces are measured in one of three ways: low efficiency, mid efficiency and high efficiency. What?s the difference? Higher efficiency models have ways to store and exchange heat while less efficient models do not. Replacing your furnace with an Energy Star furnace will cost about $1,400.

3. The Dishwasher

A typical dishwasher usually uses about 10 gallons of water per cycle! Thanks to Energy Star, however, modern, efficient dishwashers only use 5.8 gallons of water per cycle. Plus, Energy Star dishwashers tend to be quieter and clean a little better. Invest $550 in a new efficient dishwasher!

4. The Refrigerator

The refrigerator is the appliance that has made leaps and bounds when it comes to energy efficiency. The standard refrigerator now uses 40-60% less energy than it previously did in the 1990?s! The average cost of a new refrigerator is about $1,100, but you can save up to $200 a year by upgrading!

Bouns! Be sure to buy a fridge with a freezer on top. It may seem old school, but it?s more efficient than the side-by-side models!

5. The Washing Machine

The final appliance on our list is the washing machine. This machine has made vast improvements in the last few years?especially in its features. Newer washing machine models now boast front-load clothes washers which use around 50% less water and 37% less energy than top-load models. The average price of a new Energy Star washing machine is $750 and you can save over $135 a year with the upgrade!

When it comes to appliances, many of us do not upgrade until the machine breaks or is just too old to get the job done. But now?s the time to consider upgrading your appliances not only because it may be breaking down, but because it could save you money in the long run (not to mention, it saves the earth!).

The Ins-and-Outs of First Time Homeowner?s Assistance

You?ve got the car, you?ve settled into your job and you

feel like you?re finally ready to settle down.

What?s next? Now it?s time to buy a house! Owning a home for the first time a rewarding,

yet complicated process that can be drastically simplified through first time

homeowner?s assistance. But what is this

assistance all about, who qualifies and how can you get it? Team Ohlde is here to help you investigate.

What?s First Time

Homeowner?s Assistance All About?

First time homebuyer programs, such as The Johnson County Housing

Services First Time Homebuyer Program, are designed to assist

low-to-moderate income people who have been employed for at least two years in

a certain area with the purchase of a home.

Programs such as Johnson Country?s are made possible through a HOME

grant, which are given by the US

Department of Housing and Urban Development.

Who Can Get It?

If you?re interested in first time homeowner?s assistance,

you must fit in the following four categories:

If you?re interested in a first time homeowner?s assistance,

you not only have the fit the bill, but you have to be dedicated too. It?s not an easy process, but it could be

worth it in the end. The program will

require the homeowner to:

The program seems a little complicated at first. We?ll help you break it down to make it a bit

simpler. Each first time homeowner?s

assistance program is different, so we will use Johnson County as a primary

example:

There are a lot of options for first-time homeowners! These include single-family homes,

condominium units, townhouses, cooperative units and manufactured houses with

lots.

Sign Me Up! How Can I

Get Started?

To apply for a first time homeowners assistance program in

Johnson County, please click here

and fill out the application and send to:

Johnson County Housing

Services

12425 West 87th Street

Parkway, Suite 200

Lenexa, KS 66215

Good luck with the purchase of your first home! Be sure to learn more at http://hsa.jocogov.org/housing/fthba.shtml#a. To learn even more about first time

homeowner?s assistance or to start your home search right now, be sure to

contact Team Ohlde and visit us online at http://www.overlandparkhomesbytoddohlde.com.

Top School Districts in the Kansas City Area - Blue Valley USD #229 is No. 1

In looking for a home many buyer's will consider the area school districts. Here is a list published by Ingram's listing the top area school districts ranked by average ACT scores.

List of Top K.C. Area School Districts

Of the top five listed, three are in Johnson County, KS (#1 - Blue Valley School District 229, #2 - Shawnee Mission School District 512, #4 - Olathe District Schools 233). The top school district on the Missouri side of the state line is Lee's Summit R-VII coming in at #3.

Search for homes in the Blue Valley School District

Search for home in the Shawnee Mission School District

Feel free to contact me to schedule a private consultation to discuss your real estate needs.

913-568-7355

Housing Affordabilty

Housing affordabilty is at historical lows, not since the 70's has it been this affordable. Housing affordabilty is determined by looking at average housing prices along with mortgage interest rates (30 year) and determining what percentage of a homeowners monthly income is consumed by their house payment. Currently it's at 13.6% compared to 23% in 2006. Take a look at the attached slide presentation.

2012 U.S. Housing Market

Even Warren Buffet says buying single family homes in this market is better than stocks! Read his comments on CNBC.

http://www.cnbc.com/id/46538421

Take a peek at what's on the market and let me know it you'd like to get the ball rolling on finding a home.

Keep home staged and show ready for buyer inspections & appraisal

I think everyone will agree that a well staged home will increase buyer interest in a home. Research even shows that a buyer is likely to pay more for the home. The buyer's inspector and the banks appraiser are no different. If they walk into a home that's staged, clean, and ready to be shown they are naturally influenced to believe the owner has taken good care of the property and it's in above average condition. Therefore, the inspector is less likely to nit pick and the appraiser is less likely to make negative condition reductions when comparing it to other properties. So, once your home is under contract don't relax just yet. Keep the property ready for the inspector and the appraiser to reduce heartache later in the transaction.

Johnson County, KS 4th Qtr 2011 Sales Increase

Increased sales in the 4th quarter of 2012 have created a Seller's Market to begin 2012. Currently Johnson County conditions show a Seller's Market (< 5 months supply) for homes priced under $400,000 with a Balanced Market (5-7 months supply) at $400K - $500K and a continued Buyer's Market (>7 months supply) $500K+. See the attached document for more details, Jan_2012_Stats.pdf ,numbers used to calculate were pulled from Heartland MLS.

It's likely these conditions will be short lived as Spring market inventory will begin to come on the market. The question is will the increased buyer activity continue with historically low interest rates and increase consumer confidence I predict Yes. The time to act is now especially if you are a move up buyer. Call me to schedule an appointment to discuss your property and buying plans.

Just Listed! Overland Park Ranch - Blue Valley Schools

View Virtual Tour

Why Buy a Home in 2011?

Are you considering buying a home but are still on the fence? Get off it, it's time to buy. Here are a few good reasons why:

Currently inventory in Overland Park, KS is at an 8 month supply which indicates a continued strong buyer's market.

Interest rates are on the rise, view rates, as I write this 4.875% on a 30 year fixed conventional loan, last week it was as high as 5.25%. They'll most likely be above 5.0% again very soon for good.

The housing market in Overland Park, KS is back on the way up. We've seen sales of existing inventory increasing over the last 3 months and I expect the trend to continue. In a recent article on HousingPredictor.com, Overland Park, KS was predicted to be the 17th BEST real estate market in 2011, view article. This article supports the trend that our market is on the way up. If you as the buyer remain on the fence you'll miss out on a great time to buy - BUY LOW - sell high.

Owning a home is still important to your happiness and success. As cited in the Home Ownership Matters campaign by NAR the benefits of home ownership include 1) Higher Academic Achievement 2) More Cohesive Communities 3) Stronger Families 4) Improved Health & Safety 5) Stronger Economy. Sounds good to me, how about you?

Don't wait, get on the path to owning a home in 2011. I'll be hosting a FREE Home Buyer Seminar on Thursday Feb. 24th at 6:30pm, register today and get moving before it's too late. Can't make it on Feb. 24th? No problem, call 913-568-7355 or email me [email protected] and we can schedule a private buyer consultation.

I look forward to working with you soon!